Multiple linear regression (MLR)

Sep 30, 2024

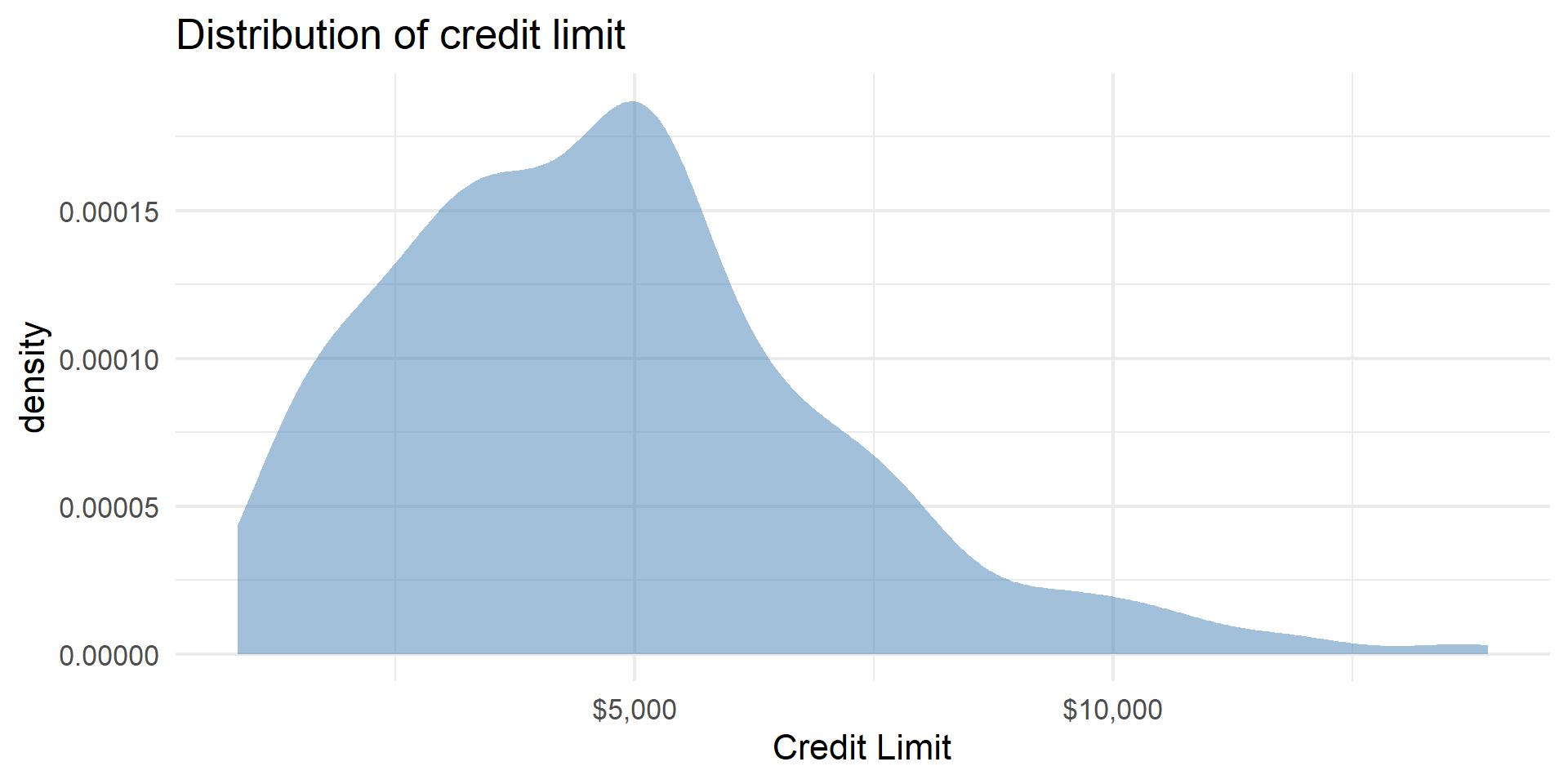

Outcome: Limit

| min | Q1 | median | Q3 | max | mean | sd | n | missing | |

|---|---|---|---|---|---|---|---|---|---|

| 855 | 3088 | 4622.5 | 5872.75 | 13913 | 4735.6 | 2308.199 | 400 | 0 |

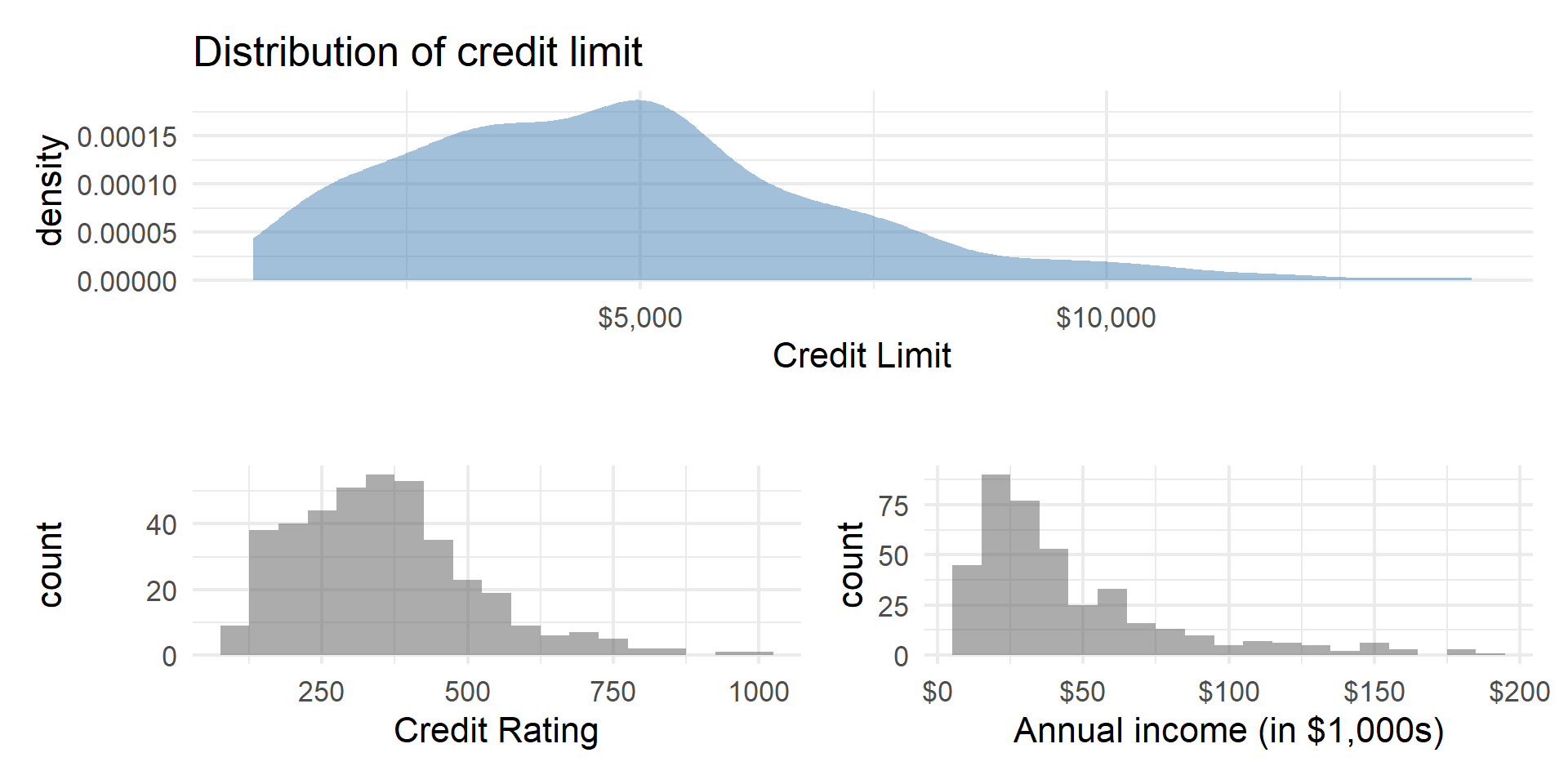

Predictors

Code

p1 <- Credit |>

gf_density(~Limit, fill = "steelblue") |>

gf_labs(title = "Distribution of credit limit",

x = "Credit Limit")|>

gf_refine(scale_x_continuous(labels = dollar_format()))

p2 <- Credit |>

gf_histogram(~Rating, binwidth = 50) |>

gf_labs(title = "",

x = "Credit Rating")

p3 <- Credit |>

gf_histogram(~Income, binwidth = 10) |>

gf_labs(title = "",

x = "Annual income (in $1,000s)") |>

gf_refine(scale_x_continuous(labels = dollar_format()))

p1 / (p2 + p3)

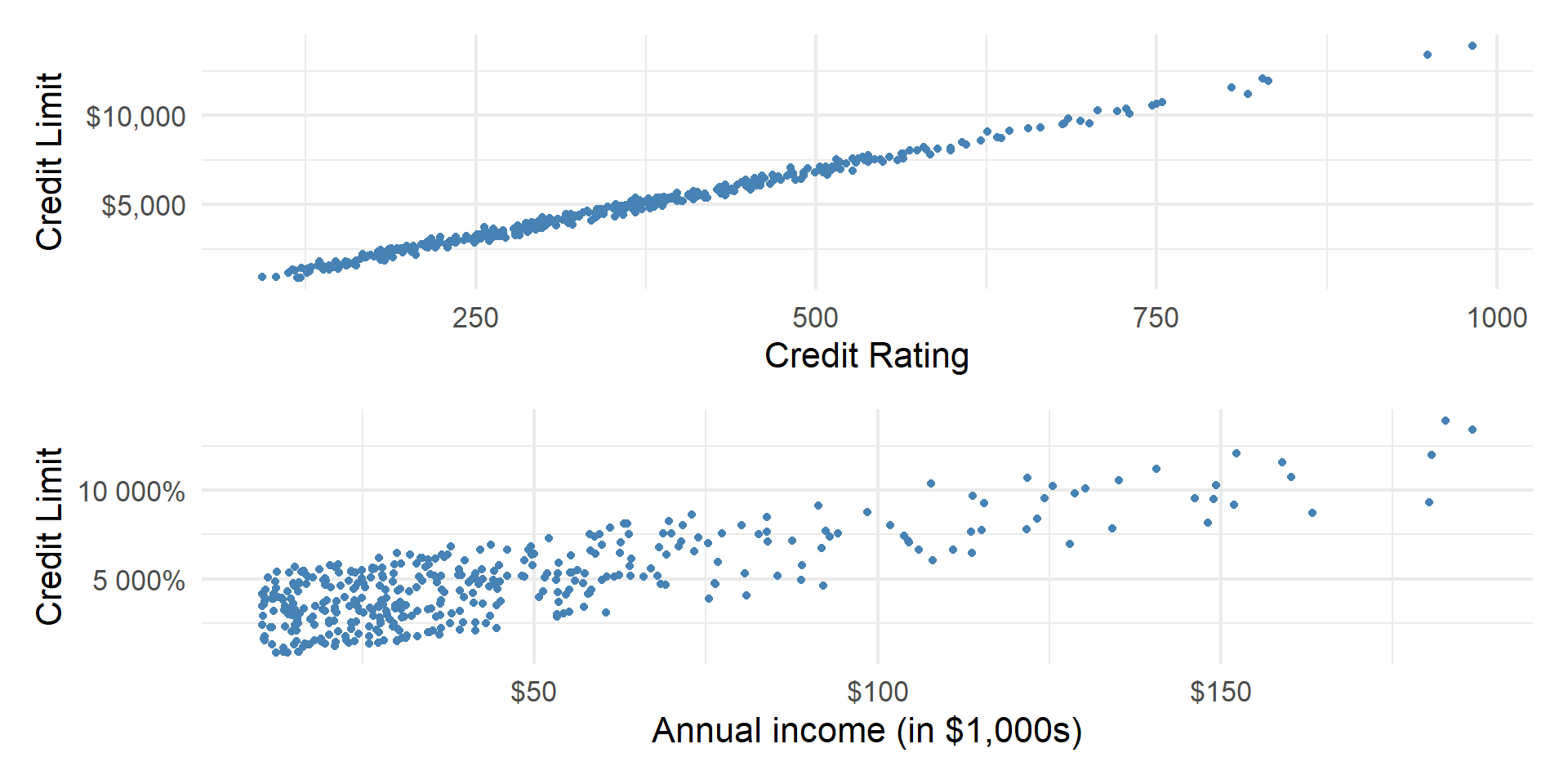

Outcome vs. predictors

Code

p4 <- Credit |>

gf_point(Limit ~ Rating, color = "steelblue") |>

gf_labs(

y = "Credit Limit",

x = "Credit Rating"

) |>

gf_refine(scale_y_continuous(labels = dollar_format()))

p5 <- Credit |>

gf_point(Limit ~ Income, color = "steelblue") |>

gf_labs(

y = "Credit Limit",

x = "Annual income (in $1,000s)"

) |>

gf_refine(scale_x_continuous(labels = dollar_format()),

scale_y_continuous(labels = percent_format(scale = 1)))

p4 / p5

Cautions

- Do not extrapolate! Because there are multiple predictor variables, there is the potential to extrapolate in many directions

- The multiple regression model only shows association, not causality

- To show causality, you must have a carefully designed experiment or carefully account for confounding variables in an observational study

![]()